![]()

|

Beginners Guide |

|

![]()

| |

Beginners Guide |

|

Note: It is important to appreciate that all derivatives are highly geared, or leveraged, transactions. Traders/investors are able to assume large positions - with similar sized risks - with very little up-front outlay. Only those that fully appreciate the risks involved should, therefore, utilise these instruments. If you have any questions relating to the following article then please e-mail ADT@ADTrading.com

Last month there were FRAs, prior to that came Financial Futures, are you ready for the challenge of Interest Rate Swaps?

Origins:

Although this product only came into existence in recent years, it can be related back to the 1800s and Ricardo's Law of Comparative Advantage. In essence, this examined two countries which both produce cloth and wine.

If country A can produce cloth more efficiently than B, then it has an absolute advantage in cloth over B. According to Ricardo's Law, however, even if A has an absolute advantage over B in both cloth and wine, that is no reason for the two not to trade.

A should concentrate on producing the commodity in which it has the greatest comparative advantage, leaving production of the other to B. The two can then trade their surplus supplies with one another, enabling them to fulfil their requirements for the commodity that they did not produce - with the net result that they are both better off.

Interest rate swaps (IRS) came into existence by applying the same Law to borrowing. In addition to the period concerned, companies have to pay different rates of interest according to:

IRS enable them to, in effect, access sources of funding at better rates than they would be able to achieve on a direct basis.

- Their credit-worthiness

- Supply and demand

The instrument is simply:

IRS DEFINITION

An agreement between two parties to exchange

stated interest obligations for a certain period

in respect of a notional principal amount.

The parties can be a bank and a customer, or two banks. Two customers dealing together would be unusual, although in these times of disintermediation perhaps it may become a possibility.

With single currency IRS, there are two possible combinations of interest obligations that can be exchanged:

- "Fixed against floating", an example of which could be 9% fixed against 6 month LIBOR.

Some banks quote prices in terms of a spread over a related instrument, such as U.S. Treasury Bonds. This is done because:

Swap prices are closely related to bonds. Market makers use such bonds,

or futures or options on them, to

hedge their positions.Some even trade just the spread,

rather than any directional view.- Floating against floating, known as "basis" swaps, which involve the exchange of two different types of floating rate, an example of which might be 6 month LIBOR against 1 month Commercial Paper rates.

They are usually priced in terms of a spread over/under one of the reference rates.

Even experienced dealers need to check certain aspects of the price for both the payment and receipt streams:

As an example of the need for this, serious problems will result if, on checking through the deal one party finds that, although it is expecting to receive 8% money market, quarterly, its counterparty believes that it will be paying 8% annual bond. (Still, what's $52,000 a year on a $10 mill. deal between friends ?!)

- Interest basis: Money market (actual/360 or 365) or

Bond (30 day month and 360 day year) ?- Periodicity: Annual, semi-annual, quarterly ?

The period is whatever is agreed at the time of the deal.

IRS are dealt for a variety of maturities ranging from one year or less through to thirty years or more. The longer maturities tend to be only available to the most credit-worthy counterparties, as credit naturally becomes more of a concern with the longer dated transactions.

It must be stressed that the principal amount is purely "notional". It exists only to facilitate the calculation of interest. There is no physical exchange of principal in single currency IRS.

IRS are most easily understood by means of a specific example:

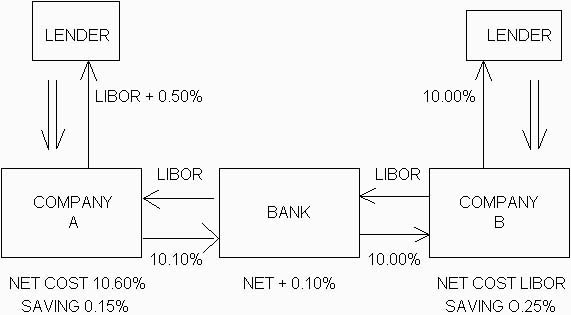

Company A can borrow: 6 month floating rate at LIBOR + 0.50%

5 year fixed rate at 10.75%It would like a fixed rate borrowing, but at cheaper rates.

Company B can borrow:

6 month floating rate at LIBOR + 0.25%

5 year fixed rate at 10.00%It would like to reduce its floating rate borrowing costs.

Company B obviously has a higher credit rating - it has an absolute advantage over A in both fixed and floating rate. It can, however, only borrow at 0.25% better in floating rate terms, whereas in fixed rate its advantage is 0.75%.

This is a typical situation - there are normally far larger differences between the rates that different credits will pay in medium or long term fixed rate borrowing than at the short end of the yield curve.

B should, therefore, borrow at the fixed rate, in which it has the greatest comparative advantage, even though it wishes to borrow at a floating rate.

It thus borrows at 10.00% fixed and, independently of this process, enters into an IRS paying LIBOR in exchange for receiving 10.00% fixed.

As can be seen from the diagram below, the 10.00% payments net out, in effect leaving B with its desired floating rate borrowing - at a rate of LIBOR flat, a saving of 25 b.p. (0.25% p.a.) on the rate it would have paid if it had borrowed directly on this basis.

A borrows at LIBOR + 0.50% and also enters into an IRS transaction, making a fixed rate payment of 10.10%, in exchange for a floating rate receipt of LIBOR.

The net effect is to leave A with its desired fixed rate borrowing - at a rate of 10.60%, a saving of 0.15% p.a.

The bank in turn earns a net 10 b.p. for assuming the credit risks on both companies (the two IRS transactions are completely independent of one another).

This is, of course, a relatively simplistic example as, amongst other things:

Nevertheless, such transactions brought the IRS market into existence and still form an important part of the base of overall activity.

- More than one bank may be involved.

- The swaps and borrowings may well take place at different times.

- A bank may run an unmatched position, either by choice or because it has difficulty arranging an offsetting transaction.

- The structure may be far more complicated.

In essence, they are "credit rating swaps", with one party using its ability to access a source of funding on attractive terms to the mutual benefit of all concerned:

- The highly rated party is effectively able to obtain cheaper floating rate funding (in the very early days up to LIBOR - 2% or even more) than it could do directly.

- The lower credit rating is effectively able to obtain fixed rate funding at a lower rate than it could do so (if at all) directly.

IRS are widely available in the major currencies and also many of the minor ones. The three to five year markets are relatively liquid, although - as mentioned above - far longer transactions are possible for the most credit-worthy participants.

Another important area is the shorter term, one and two year transactions in some of the major currencies. These are extraordinarily liquid, but are of a very different nature, being arbitrage plays against futures contracts.

Any such apparent opportunities should be treated with caution. Far fewer are actually profitable than they may appear on first sight once the:

- Costs of dealing; and the

- Assumptions which have to be made in the calculations

have been taken into account.

IRS offer a variety of trading opportunities and have numerous uses, including:

It should always be remembered, however, that IRS are a very different type of market in comparison to, say, Futures and FRAs. There is virtually never any difficulty in trading the latter during normal hours. This is normally the case with IRS as well, but even in the major currencies there can be times when it may be difficult to find a counterparty willing to trade at a realistic price.

- Effectively converting virtually any asset or liability from:

- A fixed rate to a floating rate, or vice versa; i.e.

- A medium/long term interest rate risk to a

short term interest rate risk or vice versa.- Managing long term interest rate risk.

- Accessing different types of trading opportunities.

OTHER VARIETIES OF IRS

The flexibility and possibilities afforded by this product become even more apparent when you consider just a few of the variations on the straightforward swaps considered so far.

Amortising swaps are ones where the notional principal amount on which the interest calculations are based decreases according to a pre-determined schedule.

The main demand for this type of swap is by customers of banks who wish to:

- Match repayment schedules on loans as precisely as possible.

- Manage the interest rate risk involved in predicted funding requirements, or investment programmes.

Accreting swaps are similar, except that the notional principal amount increases according to a pre-determined schedule.

"Roller Coasters", as might be imagined, combine both features. The notional principal increases and reduces during the life of the transaction, going up and down according to a schedule agreed at the time of the deal.

These are most often used in connection with long term project financing.

Forward Start swaps have become more and more commonplace. As will be obvious to you from the name, they simply involve agreement of all the details, including the price, today - the point when the deal is transacted - for an IRS that starts, say, in 6 months' time.

CROSS CURRENCY SWAPS

Are often dealt as a result of underlying positions, particularly in connection with bonds, and have a very similar structure to IRS. There are, however, some important differences:

Details

You will appreciate from the following that, in comparison to IRS, they involve a number of additional considerations, each of which have to be agreed at the time of the deal.

Interest Obligations Exchanged

These are denominated in two different currencies, the relative amounts of which are normally determined by reference to the spot rate prevailing at the start of the deal.

This results in three different possible combinations of interest obligations which can be exchanged:

- A fixed rate in one currency against a floating rate in another.

A typical example would be a transaction whereby one party paid fixed

rate DEM and received floating rate USD (with the counterparty naturally

doing the opposite in each of these two currencies).- A floating rate in one currency against a floating rate in the other, e.g.

Pay 3 month USD LIBOR against the receipt of 6 month CHF LIBOR.

- A fixed rate in one currency against a fixed rate in another, e.g.

Pay fixed rate YEN and receive fixed rate USD.

Exchange of Principal Amounts

Unlike IRS, where the principal amount is purely notional, the situation is very different with currency swaps:

- The principal amounts are always exchanged at maturity.

Each party pays to the other the principal amount on which it has been paying interest - in a similar manner to the repayment of a loan at maturity.

- They are sometimes also exchanged at the start. In such cases:

- Each party pays to the other the principal amount on which it will

be receiving interest - just as though it was disbursing a loan.

- The structure is similar to a long term forward foreign exchange

swap - the only real difference being that interest is paid on an

interim basis during the life of the deal, instead of in the form of

one net amount at maturity.- If the principal amounts are not exchanged at the start, both parties will experience horrendous foreign exchange rate risk, unless they:

- Already have underlying transactions on their books.

- Put this front leg in place by dealing in the spot market.

The diagram below summarises these points by illustrating the cash flows that take place during the life of a fixed rate DEM against floating rate USD swap:

Credit Risk

Three factors ensure that the degree of this risk is significantly greater in comparison to IRS, namely the:

In addition to such features as amortising, accreting, roller coaster and forward start, there are two specialised types of transaction:

- Exchange of principal amounts.

- Fact that the interest obligations exchanged are in different currencies.

- Consequence that the interest payments cannot be netted, even when they are due to occur on the same date.

Asset swaps

Currency swaps can be used to structure synthetic assets in a manner which may secure a number of benefits, including:

- Funding an asset in one currency with another, without:

- Having to transact a foreign exchange deal; or

- Incurring any exchange rate risk.

- Translating a beneficial rate in one currency into another.

- Achieving a floating or fixed rate of return as desired.

- Obtaining a higher yield.

- Adjusting the credit risk profile.

Diff swaps

are a hybrid of both IRS and currency swaps.

As with IRS:

- There is no exchange of principals.

- There is a single notional principal amount, e.g. DEM 50 million.

- The payments which are exchanged are denominated in one currency, e.g. DEM.

As with currency swaps:

- The interest payments which are exchanged are based on e.g.

- DEM LIBOR against

- USD LIBOR + spread,

BUT, both amounts are calculated on the DEM 50 mill. notional principal. They therefore enable companies to link the cost of borrowing in one currency to interest rates in another, without incurring any exchange rate risk.

From the bank's point of view, however, it is impossible to completely hedge all the risks incurred from these transactions.

We appreciate the assistance of AWCT, specialists in

wholesale financial markets training, in writing this Guide.

Classifieds:

Forthcoming Events

Small Ads

Column: Stutz-Auburn-Duessenburg on A

Busy Month

Competition: Last Chance to Enter The First

Risk Olympics

Contract Focus: SIMEX Nikkei 225 Index Futures

& Options

Feedback: Your

Correspondence

Question Time: Your Queries

Answered

Soapbox: Free Speech For

Derivatives?

Software Review: Derivan

Trading

Techniques: A Checklist For

The Open

The Back Page: Rearview

Back Issues: Via This Index

Glossary: Jargon Solutions Start Here...

![]()

[Reply | Subscribe Free! ]

![]()